OPINION:

The weeks before Christmas were busy in Washington, D.C. The Federal Reserve raised its benchmark interest rate by 25 basis points on Dec. 16. It was the first Fed rate hike since 2006 and, according to Federal Reserve Chair Janet Yellen, may be the first of what is likely to be a number of modest interest rate hikes over time. The real questions are how much, over what period, and with what consequences?

At the end of that week both the House and the Senate passed comprehensive tax and spending legislation with a strong bipartisan vote in both chambers. The good news is that some of the tax extenders and related additional spending had merit, and the spending legislation avoided a government shutdown. The bad news is, according to the nonpartisan Committee for a Responsible Federal Budget, the legislation is likely to increase federal deficits and debt levels by $2 trillion to $4 trillion over the next 20 years depending on the assumptions that are used regarding future congressional actions.

Higher federal deficits and debt levels just serve to reinforce the fact that the federal government will eventually need to restructure its finances, which will likely exacerbate the financial challenges of troubled states. Some states added significant debt in recent years during a period of historically low interest rates. Higher interest rates will mean higher interest expenses over time. State policymakers need to keep in mind that bad news ultimately flows downhill to lower levels of government. Importantly, states have less flexibility than other levels of government. For example, unlike at the federal level, they can’t print money or set interest rates. And unlike at the city and county level, they can’t declare bankruptcy.

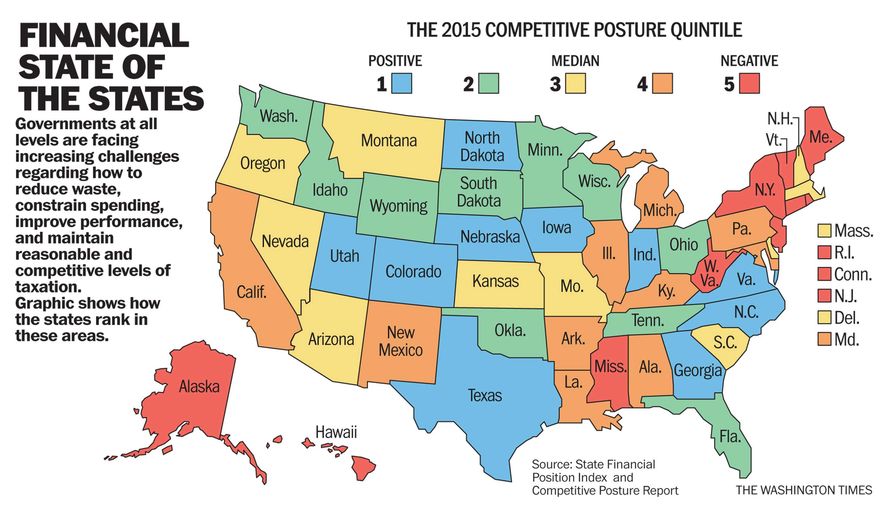

Given the above, PwC Public Sector published the State Fiscal Responsibility Index and Competitiveness Posture Report to help shed light on the relative financial position and competitive posture of each state and the degree of restructuring that may be necessary to improve both. The report shows that the financial position of the states varies widely. Eleven states had positive net positions as of June 30, 2014, even when full unfunded pension and retiree health care obligations were considered. The remaining 39 states had negative net financial positions of varying magnitudes.

The report makes clear that most of the states that rank near the top of the index tend to have smaller populations, significant natural resources, limited unfunded retirement obligations, high competitiveness rankings, and positive net migration patterns. The notable exception is Alaska, which ranks No. 1 in fiscal position but poorly in other measures. States that rank near the bottom of the index have large unfunded retirement obligations, rank in the bottom tier of states for competitiveness, and have net negative migration patterns.

State policymakers, taxpayers and other key stakeholders should check out where they stand in the new report. After all, you don’t really know how good or bad you have it until you compare your situation to others.

States that rank high should stay the course and seek to pursue continuous improvement efforts. States that rank poorly need to engage in a range of organizational, operational, financial and other reforms to improve their financial position and competitive posture over time. Financial reforms may likely include, among other things, restructuring existing retirement plans and enforced funding requirements that are fair to employees, retirees and taxpayers who have to pay the bill.

State leaders need to keep in mind that while most Americans have no desire to leave the United States, they may leave a state (absent strong family or other ties), especially when they enter their retirement years.

Defusing our structural federal debt bomb and creating a comeback in challenged states will require extraordinary leadership from the president and respective governors. It will also require meaningful public engagement to make an effective case for needed reforms and private negotiations to achieve support for such reforms. Ultimately, it will take principle-based, goal-oriented and nonpartisan solutions that can achieve meaningful bipartisan support in order to achieve sustainable success. My personal experience as a leading transformation agent within government and as a leader of citizen engagement activities around the country tells me that this approach can succeed and would create a better future for all of us. The sooner we start the better.

• David Walker is senior strategic adviser at PwC Public Sector and a former U.S. comptroller general.

Please read our comment policy before commenting.