OPINION:

In a supremely weird election season the latest weird twist is the consensus emerging on Wall Street that Hillary Clinton would be better for financial markets than Donald Trump.

The usually sensible Barrons magazine concluded its cover story last week that Hillary-onomics is better for investors than Mr. Trump. Warren Buffett and other stock gurus have made the same case.

The argument for Hillary is that she’s predictable and that Wall Street knows what she will do. Mr. Trump, by contrast, is the high beta candidate, and let’s face it: no one knows exactly what you get with a President Trump. She’s the safer bet. Investors also are drooling for a return to the 1990s and the bull market returns under Bill Clinton — when stocks tripled in value. I know I am.

Hillary is seen as less likely to spark a trade war that could send stocks tumbling.

But there’s a problem with each of these arguments. It’s true that Hillary brings far more certainty, but what this means is that we are absolutely certain to get bad ideas. I never have bought the argument that Wall Street wants the devil they know.

If you’re walking down a dark street at night and there’s a 100 percent chance that you will get mugged on the left side of the street and a 50 percent chance if you cross over to the right side of the street, what’s the logical move?

Hillary is 100 percent predictable. She is going to raise tax rates; she is going to spend trillions more over the next decade; she is going to stop drilling for oil and gas and shutdown our coal industry; she is going to double down on Obamacare; and she is going to wage war against the rich on Wall Street. Is that the certainty Wall Street is craving?

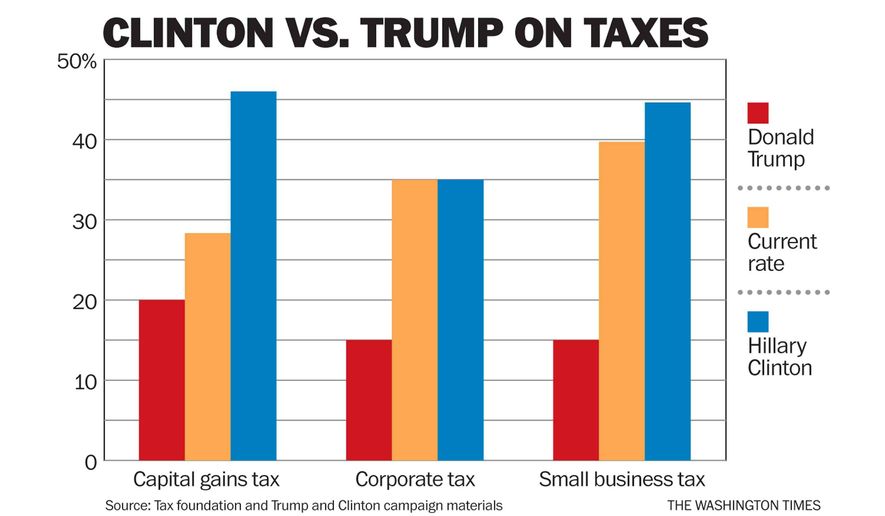

Let’s take taxes. Mr. Trump wants a 20 percent capital gains tax. Hillary wants a 46 percent capital gains tax. Now these are direct taxes on investors. What is the difference between these two policy courses? A share of stock is worth the discounted present value of the returns after tax. So let us assume a stock earns $10 a share. Under Hillary the stock’s after-tax return is $5.54 a share. Under Mr. Trump the after-tax return is $8.00. This is an oversimplification because Hillary would tax longer held stocks at a rate of 23.8 percent. But the stocks have a much higher return under Mr. Trump.

But the corporate tax also has an effect on stock values. Hillary wants to keep the 35 percent rate. Mr. Trump wants a 15 percent rate. So under Hillary the government takes one-third of corporate profits, and under Mr. Trump the government takes one-sixth of the profits. It’s true the effective tax rate is lower for many multinationals, but the broader point is obvious: Mr. Trump’s tax plan is much, much, much better for stocks than Hillary’s. By the way I didn’t even mention that Mr. Trump wants a lower estate tax — another tax on stocks — and Hillary wants a more confiscatory system.

But stocks did phenomenally well under Hillary’s husband. True but this isn’t Bill Clinton’s party anymore. Hillary is running as Bernie-lite, not Bill-lite. The days of the centrist Democrats are long past. Bill balanced budgets, cut spending, cut the capital gains tax and signed welfare reform. Hillary stands on the other side on all these issues.

On trade, Mr. Trump’s black mark, Hillary might be better, but not by much. She’s against the Asia trade deal. She was against lifting the export ban on American oil and gas.

Will there be a Hillary Clinton bull market? I’d short that bet. And in some ways, Mr. Trump could be the most pro-investor president in decades.

• Stephen Moore is an economics consultant with Freedom Works and a Fox News contributor.

Please read our comment policy before commenting.